Simple Budgeting Methods for Beginners

A first budget doesn’t need a finance degree or a complicated spreadsheet to work. Most beginners can rough out a working plan in under an hour using nothing more than a bank statement and a pen. This guide walks through the five simplest budgeting methods people actually stick with, how to pick the right one, and the steps to build the first draft today.

Start With Take-Home Pay, Not Gross Income

Every budgeting method starts with net income, the amount that actually lands in a checking account after taxes and deductions, not the higher number listed on a pay stub. Budgeting around gross income distorts the entire plan before it begins.

Someone with irregular income from freelance work or gig platforms should average the past three to six months of earnings and plan around the lower end of that range. This leaves room to adjust upward during stronger months instead of coming up short during slower ones.

Freelancers and gig workers also need to set aside a separate percentage for taxes before calculating a spendable budget, since nothing gets withheld automatically the way it does from a traditional paycheck.

The 50/30/20 Rule

The 50/30/20 method splits take-home income into 50% for needs, 30% for wants, and 20% for savings and debt payoff, making it the most forgiving option for a first-time budgeter. Popularized in Elizabeth Warren’s 2005 personal finance book, this rule doesn’t require tracking every single transaction.

Needs cover the non-negotiables: rent, utilities, groceries, minimum debt payments, and transportation. Wants cover everything enjoyable but skippable, dining out, subscriptions, entertainment, and hobby spending. The remaining 20% goes toward savings, an emergency fund, or extra debt payments.

Someone earning $4,000 a month after taxes would aim for roughly $2,000 in needs, $1,200 in wants, and $800 toward savings and debt. The percentages are a starting point, not a rigid law, and can shift based on cost of living in a given city or region.

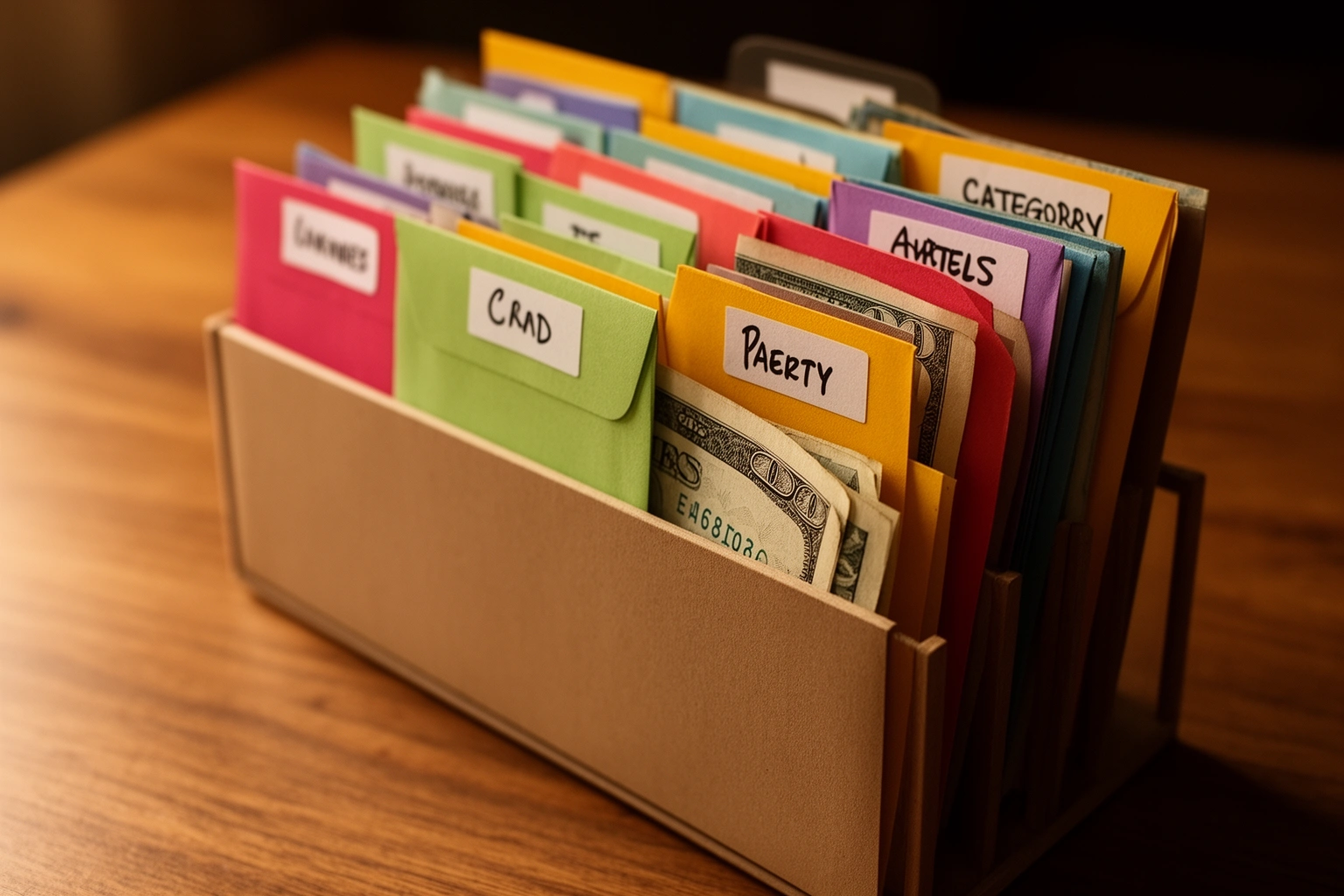

The Envelope System

The envelope method assigns a fixed cash amount to physical or digital envelopes for each spending category, and spending stops automatically once an envelope runs empty. This method suits people who overspend on categories like groceries, dining out, or shopping.

Withdraw the budgeted cash for the month, divide it between labeled envelopes, and spend only what’s inside each one. Once an envelope is empty, that category is closed until the next paycheck arrives, which removes the temptation to swipe a card for “just one more” purchase.

Digital versions work the same way through banking apps or spreadsheets for anyone who prefers not to carry physical cash. The core mechanic stays identical: a hard limit per category with zero flexibility to borrow from another envelope mid-month.

Zero-Based Budgeting

Zero-based budgeting assigns every dollar of income a specific job, bills, groceries, savings, or fun, until income minus planned spending equals exactly zero. Nothing sits unassigned at the end of the month, which appeals to people who want total visibility over their money.

List take-home income at the top, then subtract fixed expenses like rent and utilities, followed by variable costs like groceries and gas, then savings contributions. What’s left after all categories are funded gets assigned somewhere specific instead of drifting into random spending.

This method demands more discipline and detailed tracking than 50/30/20, since every category needs an assigned amount before the month starts. Beginners who dislike granular tracking often find this method frustrating within the first few weeks.

Pay Yourself First

The pay-yourself-first method treats savings as the very first bill paid each month, transferring a set amount to savings before any other expense gets covered. This approach works especially well for people who tend to procrastinate on saving until nothing is left over.

Set an automatic transfer to a savings account for the day income arrives, before rent, groceries, or anything else gets paid. Whatever remains after that transfer covers bills first, then discretionary spending.

This method can run alongside almost any other budgeting system on this list. Someone using 50/30/20 could pay themselves first for the 20% savings portion, then use the remaining 80% for needs and wants without additional tracking.

Anyone building this kind of habit around consistent, automatic saving often finds it connects naturally with the psychology covered in why some people are naturally good savers, since both come down to removing decisions rather than relying on willpower.

Which Budgeting Method Fits Which Personality

The right budgeting method is the one a beginner will actually stick with for three months, and personality matters more than which method has the most features. Matching method to temperament prevents the common pattern of quitting within the first few weeks.

| Method | Effort Level | Best For |

|---|---|---|

| 50/30/20 Rule | Low | Big-picture thinkers, first-time budgeters |

| Envelope System | Medium | Overspenders on specific categories |

| Zero-Based Budgeting | High | Detail-oriented planners |

| Pay Yourself First | Low | Procrastinators, automation lovers |

Most beginners can rough out a first working budget draft in under an hour using take-home pay and two to three months of bank statements.

Building the First Draft in Five Steps

Calculating take-home income, listing every expense, setting financial goals, choosing one method, and tracking spending for a month covers the full process from zero to a working budget. Skipping the tracking step is the most common reason first budgets fall apart within weeks.

Pull the last two to three months of bank and credit card statements and sort every transaction into fixed or variable costs. Fixed costs stay the same each month, rent and phone bills. Variable costs fluctuate, groceries and gas.

Set one short-term goal, like a $500 starter emergency fund, before tackling anything bigger. A small achievable target builds the habit of following the budget before adding the pressure of a large long-term goal.

Review the budget weekly for the first month rather than waiting until month’s end. Ten to fifteen minutes spent checking spending against the plan catches problems early enough to adjust before the whole system feels broken.

Frequently Asked Questions

What is the easiest budgeting method for beginners?

The 50/30/20 rule is typically the easiest starting method since it splits income into three broad categories without requiring every transaction to be tracked individually.

Should a budget be based on gross income or take-home pay?

A budget should use take-home pay, the amount left after taxes and deductions, since gross income includes money a person will never actually see or spend.

Can budgeting methods be combined?

Yes, the pay-yourself-first method pairs naturally with 50/30/20 or zero-based budgeting by treating the savings portion as the first transfer made each month.

How long does it take to build a first budget?

Most beginners can build a rough first draft of a working budget in under an hour using take-home income and two to three months of bank statements.

Is a budgeting app better than a spreadsheet for beginners?

A budgeting app works well for people who don’t enjoy manual data entry and want automatic syncing, while a spreadsheet or envelope system suits people who want full control over categories.

What is a good first savings goal when starting a budget?

Building a small starter emergency fund of $500 to $1,000 is a common first goal, since it prevents one surprise expense from derailing months of budgeting progress.